How Open Finance Brasil’s Credit Portability API Works: End-to-End Process and Impact

The Open Finance Brasil ecosystem has reached another major milestone.

Following the successful rollouts of data sharing and payments APIs, the Credit Portability API has now entered its production pilot phase, bringing with it the promise of greater competition and transparency in Brazil’s credit market.

The Credit Portability API allows consumers to transfer existing credit or lease agreements between financial institutions in search of better conditions – fully online, in as little as five days, a quarter of the time previously required. Initially focused on unsecured personal loans, the feature is expected to expand to other credit products in the near future.

This new capability represents one of the main deliverables for 2025–2026 within the Open Finance Brasil program.

How Open Finance Brasil’s Credit Portability API Works

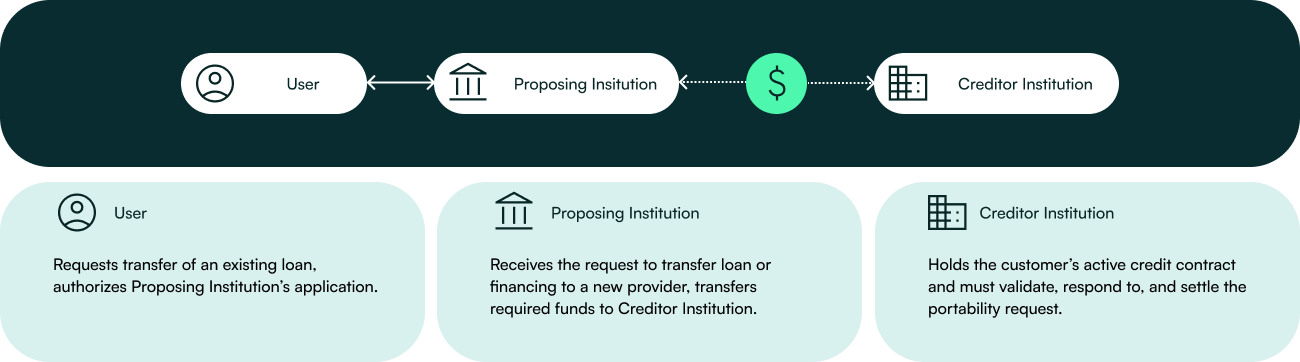

At the center of the Credit Portability process are two main participants:

-

The Proposing Institution, which receives the customer’s request to transfer an existing loan or financing to a new provider.

-

The Creditor Institution, which currently holds the customer’s active credit contract and must validate, respond to, and settle the portability request.

Both institutions interact securely through standardized APIs defined under the Open Finance Brasil FAPI profile, using digital certificates, signed payloads, and token-based authentication.

Depending on the nature of the interaction, APIs can be called using either the authorization code or client credentials grant types.

When the authorization code flow is used, it follows the same scopes defined for Data Sharing (Loans APIs)–meaning that the portability journey begins with a data sharing flow.

If the customer has already shared loan data, that existing consent can be reused; otherwise, a new consent and redirection are initiated so the user can authorize the data access.

From this point onward, all subsequent steps in the portability process are fully automated between the two institutions.

1. Data Sharing and Contract Retrieval

The journey starts when the customer, through the Proposing Institution’s application, authorizes the sharing of their existing loan information from the Creditor Institution. This occurs via the standard Data Sharing flow of Open Finance Brasil, allowing the proposing institution to retrieve the relevant loan contracts that may be eligible for portability.

2. Data Sharing and Contract Retrieval

Endpoint: GET /credit-operations/{contractId}/portability-eligibility

With access to the contract information, the Proposing Institution checks whether a specific loan is eligible for portability. This endpoint, exposed by the Creditor Institution, returns the eligibility details that confirm whether the contract meets the regulatory and technical conditions to be ported.

3. Portability Request Submission

Endpoint: POST /portabilities

If the contract is eligible and the customer decides to proceed, the Proposing Institution submits a portability request to the Creditor Institution. This request contains all necessary information about the new loan offer (such as rate, term, and total amount) and is digitally signed to ensure integrity and non-repudiation. The Creditor Institution receives this proposal and evaluates it – either matching the conditions or rejecting the portability request.

4. Portability Status Monitoring

Endpoint: GET /portabilities/{portabilityId}

Throughout the process, the Proposing Institution can monitor the current status of the request. This endpoint allows it to track the flow from submission through acceptance and settlement, providing transparency to both the institution and the customer.

As defined in the specification, the Creditor Institution may also issue a counterproposal–offering revised loan conditions that could be more advantageous to the customer. In such cases, the counterproposal is presented directly to the user via the Creditor Institution’s own application, where the customer can review the new offer and decide whether to accept it (allowing the portability to proceed under new terms) or reject it (continuing with the portability initiated by the Proposing Institution).

5. Payment Settlement

Endpoint: POST /portabilities/{portabilityId}/payment

Once the Creditor Institution accepts the portability, the Proposing Institution proceeds with the financial settlement. This involves transferring the required funds to the creditor outside of the Open Finance infrastructure, through Brazil’s existing Reserve Transfer System (STR) – the standard mechanism used by financial institutions to transfer reserves held at the Central Bank.

The settlement confirmation is then used to notify the Creditor Institution that the payment has been completed and the portability process can be finalized. At this point, the Creditor Institution closes the original credit contract, and the Proposing Institution assumes the new one under the agreed conditions.

6. Portability Cancellation

Endpoint: PATCH /portabilities/{portabilityId}/cancel

Before settlement, the Proposing Institution or the customer may cancel the portability process. This endpoint ensures both parties – proposing and creditor institutions – update the request’s status and prevent any further actions or fund transfers.

Each interaction throughout this process is digitally signed and validated against a strict set of rules – ranging from security to functional validations. These include certificate and access-token checks, signature verification, idempotency control, and consistency across financial fields and identifiers.

Together, these measures guarantee secure interoperability and consumer protection across the ecosystem.

Raidiam’s Role in Credit Portability

Raidiam has been a proud partner of Open Finance Brasil since its inception, supporting the governance structure and technical foundation of the ecosystem.

For the Credit Portability initiative, Raidiam’s contributions span three critical layers:

Specification Review and Advisory

Raidiam’s engineers and product experts collaborated closely with the Open Finance Product Groups, reviewing specifications and providing security recommendations–to ensure full adherence to the FAPI Advanced Security Profile.

Certification Tool Development

Before participating in the production pilot, all institutions must first pass through Raidiam’s Conformance Suite– the mandatory certification platform that validates each implementation against the official API standards. Only once an institution successfully completes this certification process can it move forward to participate in the pilot stage.

Production Validation Platform (FVP)

Once the pilot starts, the Production Validation Platform becomes one of its core components. It enables institutions to execute real interoperability tests directly in production environments, using real user data to validate both happy and unhappy paths. This ensures that once institutions move to live operations, their systems behave consistently, securely, and in accordance with regulatory expectations.

The Challenge of Testing an Asynchronous Journey

Unlike payment initiation or consent-based data sharing, credit portability is inherently asynchronous.

It spans multiple days and involves a sequence of states, requiring continuous coordination between proposing and creditor institutions.

Testing such a multi-step journey presented a unique challenge. To address this, Raidiam leveraged and extended one of its recent innovations – the Test Scheduler.

Originally introduced to automate tests for scheduled payments, the Test Scheduler now plays a pivotal role in credit portability validation.

It allows the execution of time-dependent test sequences within the same portability flow, automatically managing service desk tickets and notifying participants whenever any deviation or misbehavior is detected.

This approach not only enables end-to-end asynchronous testing but also ensures faster feedback cycles and better operational insight for participants.

Trust, Security, and the Future of Open Finance Brasil

Beyond certification and validation, Raidiam also operates the Directory–the Trust Framework of Open Finance Brasil.

The Directory ensures that only accredited participants, verified certificates, and trusted endpoints are authorized to exchange data within the ecosystem.

This trust infrastructure is what enables the Credit Portability API to operate safely, ensuring the integrity and privacy of every portability transaction.

As the pilot progresses toward its full rollout in early 2026, the Credit Portability API is set to become one of the most transformative deliverables of Brazil’s Open Finance ecosystem – giving consumers unprecedented control over their credit relationships and creating a more competitive, transparent financial landscape.

At Raidiam, we’re proud to play a key role in this journey–connecting trust, innovation, and interoperability to bring Open Finance to life.

To learn more about how Raidiam can support your Open Finance initiatives, get in touch with our team.